Managing personal finances can feel overwhelming, especially if you’re just starting out. However, using a weekly budgeting approach instead of a monthly one can make things much easier to control and understand.

A 2023 NerdWallet survey found that 84% of people with monthly budgets still overspend, showing how difficult it is to stay on track over a long period. Weekly budgeting solves this by giving you frequent check-ins, helping you adjust quickly and avoid financial mistakes.

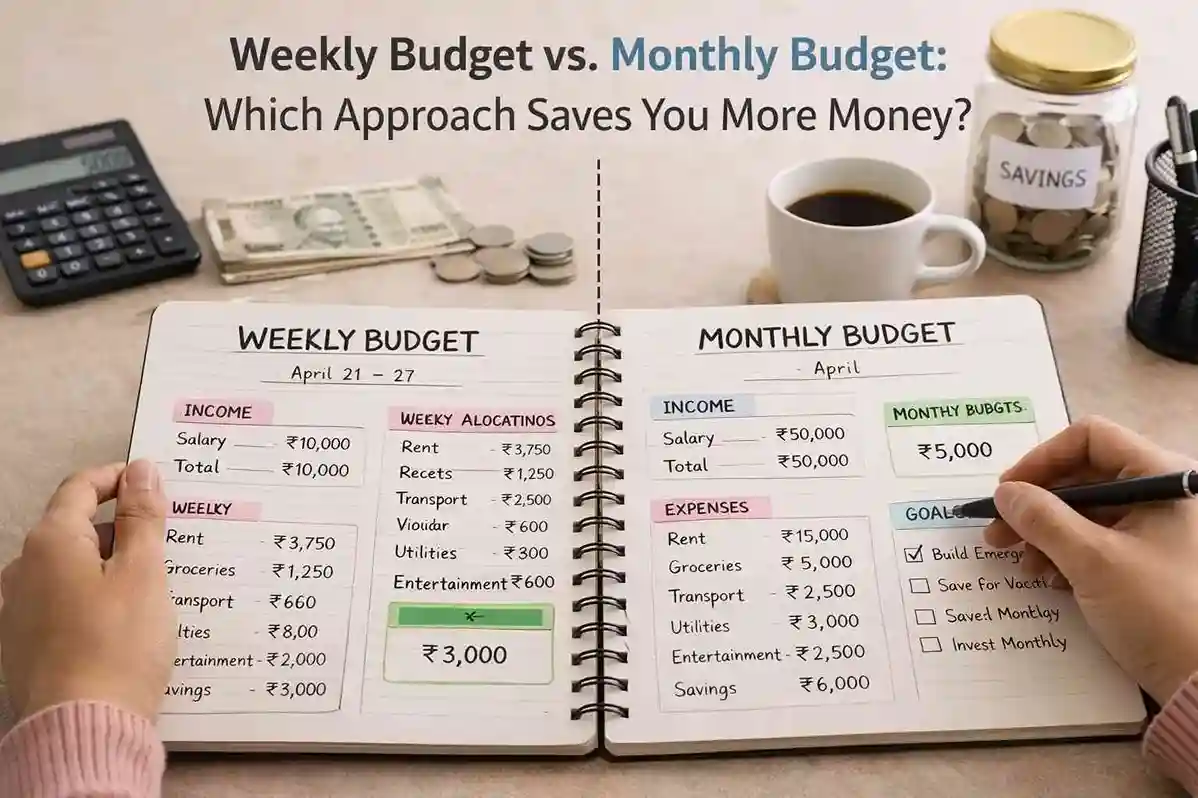

1. What Is a Weekly Budget?

A weekly budget is a short-term financial plan where you track income and expenses every 7 days instead of monthly.

This approach helps you:

- Monitor spending more closely

- Catch problems early

- Adjust quickly

Instead of realizing overspending at the end of the month, you can fix it within days.

2. What Makes a Good Weekly Budget?

A good weekly budget should be:

- Realistic – based on your actual income

- Balanced – covers needs, wants, and savings

- Flexible – handles unexpected expenses

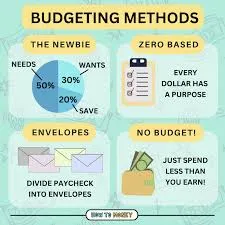

The 50/30/20 Rule (Weekly Version)

Example with $800/week income:

- $400 → essentials

- $240 → wants

- $160 → savings/debt

Consistency matters more than perfection. Over time, this builds strong financial habits.

3. Why Choose Weekly Budgeting?

3.1 Better Spending Control

You can track money closely and correct mistakes early.

3.2 More Flexibility

Unexpected costs (repairs, gifts) are easier to handle weekly.

3.3 Clearer Spending Awareness

You see patterns like:

- “$45/week on coffee” feels more real than “$180/month”

4. Weekly vs Other Budgeting Methods

| Type | Pros | Cons | Best For |

|---|---|---|---|

| Daily | Maximum control | Time-consuming | Strict spenders |

| Weekly | Flexible, clear tracking | Needs regular updates | Most people |

| Monthly | Simple, aligns with bills | Easy to overspend | Stable income |

| Biannual | Big-picture planning | Low control | Long-term planners |

5. How to Create a Weekly Budget (5 Steps)

Step 1: Calculate Weekly Income

- Use net income (after tax)

- For irregular income → use lowest average

Step 2: List Expenses

Fixed expenses:

- Rent

- Utilities

- Subscriptions

Variable expenses:

- Groceries

- Transport

- Entertainment

Convert monthly costs into weekly amounts.

Step 3: Set Savings Goals

- Save a fixed amount weekly

- Even $10/week = $520/year

- Create an emergency fund

Step 4: Allocate Your Money

- Cover essentials first

- Then savings

- Then wants

Example:

- Income: $500

- Expenses: $450

- Remaining: $50

Step 5: Track and Adjust Weekly

- Spend 10–15 minutes each week reviewing

- Fix overspending immediately

- Adjust categories gradually

Weekly Budget Example

Income: $800/week

| Category | Amount |

|---|---|

| Needs | $400 |

| Wants | $240 |

| Savings | $160 |

If you overspend one week, reduce the next — simple and flexible.

6. Special Cases

6.1 Irregular Income

- Track every payment

- Prioritize essentials

- Save more during high-income weeks

- Use percentages instead of fixed amounts

6.2 Unexpected Expenses

- Save $10–$20/week for emergencies

- Add a “miscellaneous” category

- Review weekly to stay in control

6.3 Weekly Paycheck Strategy

- Divide monthly bills into weekly portions

- Use zero-based budgeting (every dollar has a job)

- Try the cash envelope system

7. Tools for Weekly Budgeting

Templates:

- Microsoft Create

- Google Docs / Excel planners

Apps:

- YNAB

- EveryDollar

- Simplifi

- Goodbudget

These tools help automate tracking and make budgeting easier.

8. Tips for Adjusting Your Budget

- Review spending regularly

- Keep flexibility (5–10% buffer)

- Update goals when income changes

- Watch emotional spending

- Make small adjustments instead of big changes

9. Conclusion

Weekly budgeting gives you:

- Better control

- Faster feedback

- Less stress

It’s not about being perfect — it’s about staying aware and improving over time.

Start small, stay consistent, and adjust as needed. Over time, you’ll build strong financial habits and gain confidence in managing your money.