You’ve Budget probably come across the 50/30/20 rule on social media or in personal finance discussions. It’s often presented as an easy, almost foolproof way to manage money: divide your income into three parts—needs, wants, and savings.

But today’s reality is different. With inflation steadily increasing the cost of living, many people are wondering: Is this rule still realistic? Can you really stick to spending 50% on essentials when rent, food, and utilities keep rising?

The short answer: yes, but with flexibility. Let’s break it down.

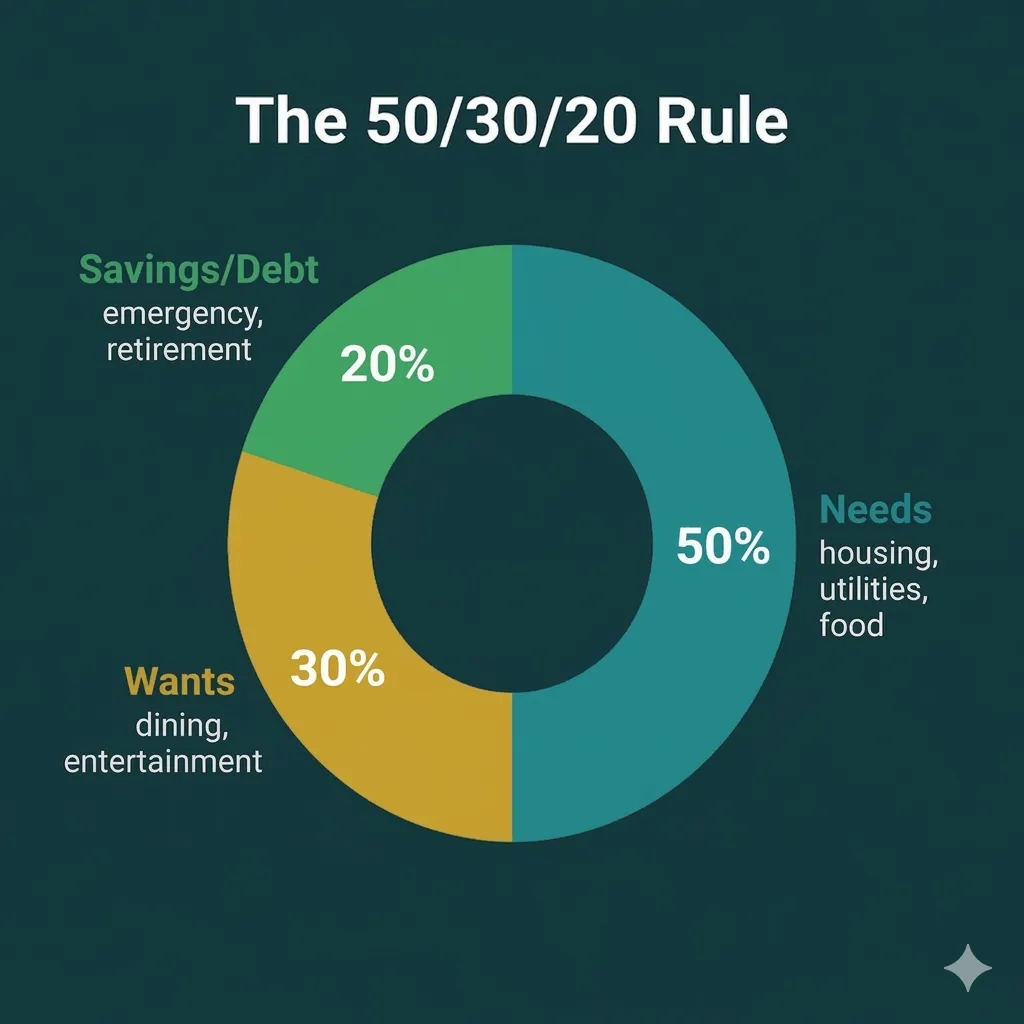

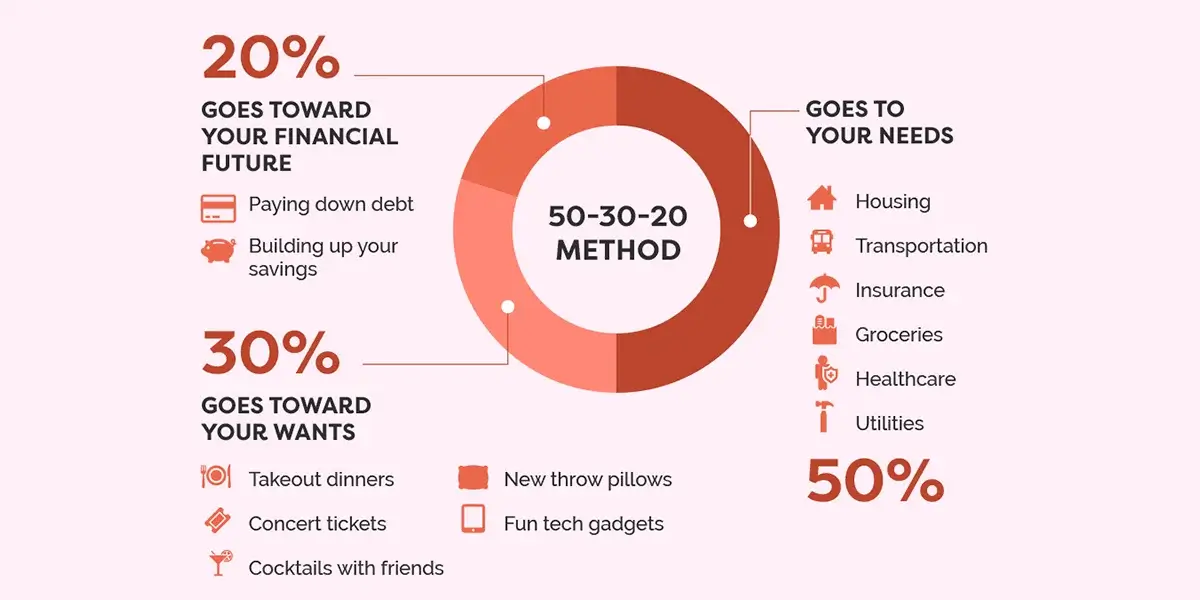

How the 50/30/20 Rule Works

At its core, the rule is simple. You divide your after-tax income into three categories:

50% for Needs

These are your essential expenses—things you can’t avoid:

- Rent or mortgage

- Utilities (electricity, water, internet)

- Groceries

- Transportation

- Loan repayments

The idea is to keep these costs at or below half your income. In theory, this creates room for saving and enjoying life. In practice, especially in expensive cities, this can be difficult.

20% for Savings

This portion goes toward building your financial future:

- Emergency fund

- Retirement savings

- Investments

- Debt repayment beyond minimums

Even small, consistent contributions matter. Automating transfers to a savings account can make this habit easier and more reliable.

30% for Wants Budget

This is your lifestyle spending:

- Eating out

- Travel

- Entertainment

- Hobbies

This category is important—it keeps your budget sustainable. Cutting out all enjoyment often leads to burnout and overspending later.

Why People Like This Rule

The strength of the 50/30/20 rule lies in its simplicity. It gives you:

- A clear structure

- Easy-to-remember guidelines

- A built-in focus on saving

For beginners or those overwhelmed by budgeting, it acts like a roadmap.

Where It Struggles Today

1. Low Income Challenges

If your income is limited, essentials alone may exceed 50%. That leaves little or nothing for savings or wants, making the rule feel unrealistic.

2. High Cost of Living

In major cities, housing and basic expenses can easily take up 60–70% of income. This shifts the entire balance.

3. Inflation Pressure

Rising costs—especially for food, energy, and housing—mean “needs” are consuming a larger share of income than before. Salaries often don’t increase at the same pace.

Adapting the Rule to Real Life

Instead of forcing the rule, treat it as a flexible framework.

Example: A Young Couple

Imagine Emma and Hugo, living in a large city with an average income. Their fixed costs (rent, bills, loans) already exceed 50%.

Rather than forcing the standard model, they adjust:

- 60% for needs

- 15% for savings

- 25% for wants

This version works better for their situation while still maintaining balance.

Practical Tips to Make It Work

- Start small with savings

Even 10–15% is a strong beginning. Consistency matters more than perfection. - Review fixed expenses regularly

Cancel unused subscriptions, compare service providers, and optimize bills. - Keep some room for enjoyment

A budget that’s too strict often fails in the long run. - Adjust without guilt

The rule is a guide—not a law. Your reality comes first.

A More Realistic Approach Today

Depending on your situation, your version of the rule might look different:

- Lower income:

70% needs / 20% savings / 10% wants - Higher income:

40% needs / 20% savings / 40% wants

The key is not hitting exact percentages—but maintaining balance and control.